Privacy is the outer skin of the self.

Privacy is the space that defines the will of the individual, which sets the area which says, ‘this is mine, because this is me.’

I may wish to share my space to varying degrees with family, friends, and acquaintances. I may even wish to operate within my space in a continuing act of worship and companionship with my Creator. But that choice to conform myself to His will and open my thoughts and heart to Him, is mine. This is a gift that is hard to comprehend, but which makes us the objects of His love, rather than a puppet, or a mere object of His to be owned.

It is His most supreme condescension that He grants us the power to resist Him, to be other than Him if we so choose. He makes us the sovereigns of a portion of His being, and says, you are free, and in His caring for another grants us a soul of our own. This is the essence of our being.

What love is that which is in thrall to the beloved, which has no choice, no self identity that it may give, freely? What are we to an all-powerful God, except that which He has granted to us, forever, as ours alone?

A tyrannical State, which has no virtuous restraint, by its very definition wishes to insert itself into this space, not as a gracious God who grants me the will to either open or close my heart to Him, but rather to take by force that space that marks my individuality, and to be as a god on its own terms.

Surveillance on an indiscriminate and massive scale by an increasingly intrusive State is not a benign act in the cause of homeland protection.

It is an act of the will to power of the State over the individual, to claim that last bastion of privacy that marks the least amount of space that a person may occupy as their own.

It is the State’s way of asserting that all that we have, all that we are, all that we may do or think, belongs to them at their unquestioned discretion.

This post was published at

Jesses Crossroads Cafe on 12 OCTOBER 2014.

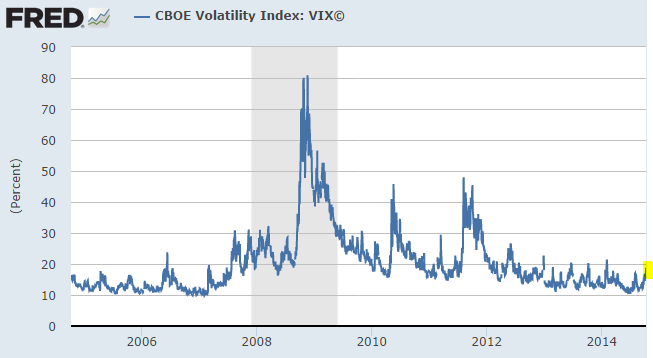

The Global stock market selloff accelerated on Friday with the FTSE 100 index falling 91.56 points, or 1.4pc, to 6,340.2, it’s lowest level in a year and 7.81pc below highs of 6,878 on May 14.

The Global stock market selloff accelerated on Friday with the FTSE 100 index falling 91.56 points, or 1.4pc, to 6,340.2, it’s lowest level in a year and 7.81pc below highs of 6,878 on May 14.

Follow on Twitter

Follow on Twitter

Recent Comments