The following video was published by FinanceAndLiberty.com on Nov 24, 2014

Gold Daily and Silver Weekly Charts – Quiet Options Expiration on the Comex

Today was the last option expiration for 2014 Comex precious metal options.

Today was the last option expiration for 2014 Comex precious metal options.

Gold and silver were under slight pressure most of the day, but closed largely unchanged. Gold was down about five dollars while silver was up a penny.

Let’s see how the trade winds down this week.

A nor’easter is expected to work its way up the east coast of the US this week. There is some uncertainly but we may be seeing a substantial winter storm in the New Jersey-New York-New England area on Wednesday, so I would expect the adults to leave on Tuesday for a long holiday weekend. The Wednesday before Thanksgiving is the biggest travel day of the year.

This post was published at Jesses Crossroads Cafe on 24 NOVEMBER 2014.

US Troops Remain In Poland And The Baltic States For WWIII- Episode 526

The following video was published by X22Report on Nov 24, 2014

Business activity tumbles to 7 month lows. More Americans can not make the payments on their cars and delinquencies are rising. The Netherlands wants their gold back and other countries will follow. 40 countries will be joining the Eurasian Union. Another banker has been found dead. Ferguson grand jury has made a decision, be prepared for an event to go hot. US keeping troops in Poland and the Baltic States in preparation for the next war. Ukraine suspends coal delivery from Russia. Unidentified jet bombs again in Libya. New malware discovered that is extremely advanced and can see everything on all systems. NORAD planning to fly over the capital with F–16s.

Global Business Confidence Collapses To Post-Lehman Lows

As we noted here, despite record high stock prices and talking-heads imploring investors to believe CEOs are confident, they are not (consider the clear indication of a lack of economic confidence from tumbling capex and soaring buybacks), That is further confirmed today as Markit’s survey of over 6000 firms showed optimism falling sharply in October, dropping to the lowest seen since the survey began five years ago. Hiring and investment plans were also at or near post-crisis lows, while price expectations deteriorated further. More worrying, perhaps, is the US is not decoupled whatsoever, with future expectations of US business activity at the lowest since the financial crisis.

As we noted here, despite record high stock prices and talking-heads imploring investors to believe CEOs are confident, they are not (consider the clear indication of a lack of economic confidence from tumbling capex and soaring buybacks), That is further confirmed today as Markit’s survey of over 6000 firms showed optimism falling sharply in October, dropping to the lowest seen since the survey began five years ago. Hiring and investment plans were also at or near post-crisis lows, while price expectations deteriorated further. More worrying, perhaps, is the US is not decoupled whatsoever, with future expectations of US business activity at the lowest since the financial crisis.

This post was published at Zero Hedge on 11/24/2014.

Twitter “Hedge Fund Manager” Anthony Davian Sentenced To 4 Years 9 Months In Federal Prison

a year ago we reported that one of Twitter early and most aggressive self-promoters, Anthony Davian, was busted for what was at the time financial Twitters’ the first Ponzi Scheme. In our words then:

a year ago we reported that one of Twitter early and most aggressive self-promoters, Anthony Davian, was busted for what was at the time financial Twitters’ the first Ponzi Scheme. In our words then:

Once upon a time there was a Twitter-based, pump-and-dumping daytrading bucket shop posing as a “successful hedge fund manager” also known as Davian Letter/Davian Capital Advisors run by an Ohio gentleman known as Anthony Davian, which for reasons unknown even managed to run outside capital (somehow raking up to $1.5 million in idiot AUM, mostly courtesy of his very aggressive self promotion on Twitter using the @hedgieguy handle), and which didn’t like Zero Hedge much.

(but that’s ok because the feeling was mutual – we had advised the SEC in late 2009 that the Davian operation was nothing but a ponzi scheme).

A few years later, said outside capital is gone (with losses that could have been prevented had the SEC moved earlier) and moments ago, following a four year delay since our notice, the SEC has finally acted and charged Anthony Davian with fraud.

Today, we can close the case on Athony Davian.

As SIRF reports, “Anthony Davian, a once-prolific presence on social media who held himself out as a iconoclastic hedge fund manager prior to his August 2013 indictment on a series of fraud charges, was sentenced several hours ago in a Cleveland courtroom to four years and nine months in federal prison.”

The details of the sent

This post was published at Zero Hedge on 11/24/2014.

Another Keynesian Debt Boondoggle: How Brussels Plans To Turn $26 Billion Into $390 Billion

The desperation and fraud of the Keynesian policy apparatus gets more stunning by the day. Apparently, the pettifoggers in Brussels will soon be announcing a new $400 billion bazooka to blast the euro-economy out of its lethargy. This massive new ‘stimulus’ is supposed to spur all manner of infrastructure and private investment that is purportedly bottled-up for want of cheap capital in the private markets.

The desperation and fraud of the Keynesian policy apparatus gets more stunning by the day. Apparently, the pettifoggers in Brussels will soon be announcing a new $400 billion bazooka to blast the euro-economy out of its lethargy. This massive new ‘stimulus’ is supposed to spur all manner of infrastructure and private investment that is purportedly bottled-up for want of cheap capital in the private markets.

Are they kidding? Thanks to the Draghi Put (‘whatever it takes’) and the hedge fund gamblers who have gone all-in front running the promised ECB bond-buying campaign, this very morning the corrupt and bankrupt government of Spain can borrow all the money it could possibly need for infrastructure at hardly 2.0% for ten years. And any healthy German exporter or machinery maker can borrow at a small spread off the German 10-year bond which is trading at 73 basis points. For all intents and purposes, sovereigns of any stripe and reasonably healthy businesses in most parts of Europe can access capital at central bank repressed rates which are tantamount to free money.

And, yet, these fools want to bring coals to Newcastle. Well, its actually worse than that because not only does Newcastle not need any coal, but the impending ‘Juncker Plan’ doesn’t include any new coal, anyway!

In fact, not a penny of the $400 billion is new EU cash: Its all about leverage and sleight-of-hand. Thus, having apparently failed to notice that most of the sovereigns which comprise the EU are already bankrupt, the Brussels bureaucrats plan to conjure this new ‘stimulus’ money at a 15:1 leverage ratio. That is to say, the actual ‘capital’ under-pinning approximately $375 billion in new EU borrowings amounts to only $26 billion.

But wait. The EU is self-evidently broke – that’s why its dunning Mr. Cameron and even its Greek supplicants for back taxes – so where is it going to get the $26 billion of ‘capital’? Needless to say, an empty treasury has never stopped Keynesian bureaucrats from dispensing the magic elixir of ‘stimulus’ money.

This post was published at David Stockmans Contra Corner on November 24, 2014.

Fed “Mystified” Why Millennials Still Live at Home; My Answer May Surprise You (It Isn’t Jobs, Student Debt, or Housing)

A New York Fed research paper wonders What’s Keeping Millennials at Home? Is it Debt, Jobs, or Housing?

A New York Fed research paper wonders What’s Keeping Millennials at Home? Is it Debt, Jobs, or Housing?

The paper says “it’s a mystery” why the housing recovery did not have a bigger impact on millennials living at home.

The research paper, written by Zachary Bleemer, Meta Brown, Donghoon Lee, and Wilbert van der Klaauw notes correlations to debt, jobs and housing.

Yet, “student debt only explains about 10% of the increase in parental coresidence since 2004, with another 10% being explained by house prices during the mid-2000s“.

I have the answer below, but first a few charts and notes on the charts.

Notes:

CCP is the Federal Reserve Bank of New York’s Equifax-Sourced Consumer Credit Panel CPS is the Current Population Survey, a joint effort between the Bureau of Labor Statistics and the Census Bureau

This post was published at Global Economic Analysis on November 24, 2014.

The Tragedy Of Propping Up The Matrix Of Lies

Wall Street is only one of several financial roach motels in what has become a giant slum of a global economy. Notional ‘money’ scuttles in for safety and nourishment, but may never get out alive. Tom Friedman of The New York Times really put one over on the soft-headed American public when he declared in a string of books that the global economy was a permanent installation in the human condition. What we’re seeing ‘out there’ these days is the basic operating system of that economy trying to shake itself to pieces.

Wall Street is only one of several financial roach motels in what has become a giant slum of a global economy. Notional ‘money’ scuttles in for safety and nourishment, but may never get out alive. Tom Friedman of The New York Times really put one over on the soft-headed American public when he declared in a string of books that the global economy was a permanent installation in the human condition. What we’re seeing ‘out there’ these days is the basic operating system of that economy trying to shake itself to pieces.

The reason it has to try so hard is that the various players in the global economy game have constructed an armature of falsehood to hold it in place – for instance the pipeline of central bank ‘liquidity’ creation that pretends to be capital propping up markets. It would be most accurate to call it fake wealth. It is not liquid at all but rather gaseous, and that is why it tends to blow ‘bubbles’ in the places to which it flows. When the bubbles pop, the gas will tend to escape quickly and dramatically, and the ground will be littered with the pathetic broken balloons of so many hopes and dreams.

All of this mighty, tragic effort to prop up a matrix of lies might have gone into a set of activities aimed at preserving the project of remaining civilized. But that would have required the dismantling of rackets such as agri-business, big-box commerce, the medical-hostage game, the Happy Motoring channel-stuffing scam, the suburban sprawl ‘industry,’ and the higher ed loan swindle. A

This post was published at Zero Hedge on 11/24/2014.

REALIST NEWS – Now the Swiss Want Their Gold Back

The following video was published by jsnip4 on Nov 24, 2014

Deutsche Bank’s Modest Proposal To Central Banks: “Purchase The Gold Held By Private Households”

From the bank that a few days ago informed us that “People Are Talking About Helicopter Money And Debt Cancellation Being The End Game“, comes the logical next step. Here it is, without commentary and the key section highlighted:

From the bank that a few days ago informed us that “People Are Talking About Helicopter Money And Debt Cancellation Being The End Game“, comes the logical next step. Here it is, without commentary and the key section highlighted:

From Deutsche bank Behavioral Finance: Daily Metals Outlook

Although gold market operators are currently pre-occupied with the prospect of the SNB finding itself obliged by referendum to buy large quantities of bullion, another central bank raised the same possibility yesterday: the ECB.

This post was published at Zero Hedge on 11/24/2014.

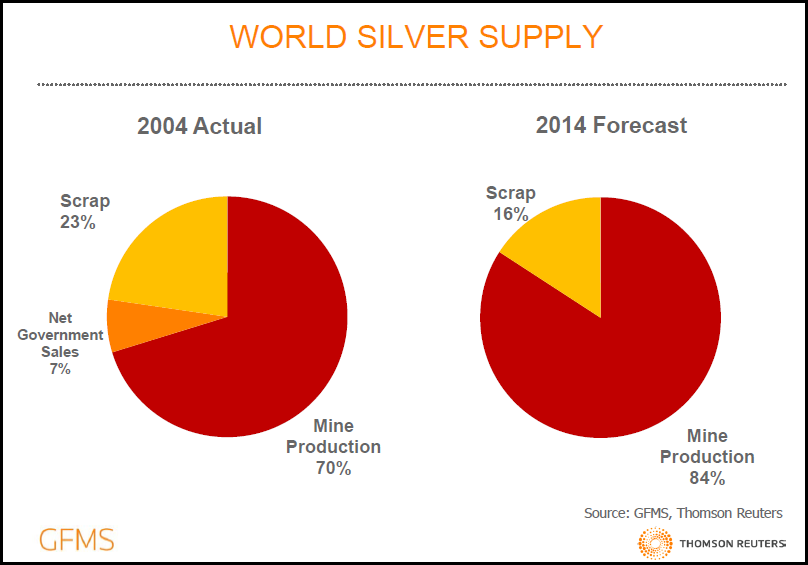

BREAKING: Significant Drawdown Of U.K. Silver Inventories Due To Record Indian Demand

There was a huge development in the silver market last week and how did the precious metal community respond? They basically ignored it. Go figure. So, I will try again to get the word out by presenting it in a different fashion.

There was a huge development in the silver market last week and how did the precious metal community respond? They basically ignored it. Go figure. So, I will try again to get the word out by presenting it in a different fashion.

Indian silver demand was so strong this year, that it produced a significant drawdown of U. K. silver inventories. Matter-a-fact, India had to access silver from China and Russia because available supplies from the U. K. were not sufficient.

According to GFMS Silver Interim Report released on Nov 18th:

Meanwhile demand for silver bars and coins has soared in recent weeks as bargain hunting retail investors returned to the silver market after a disappointing first half of the year. Nowhere is this more evident than in India where imports of silver are up by 14% year-on-year for the January to October period and set for an annual record. With imports in the first ten months totalling a massive 169 Moz many vaults in the UK, traditionally the largest supplier to India, have seen significant drawdowns, leading to more supply flowing from China and Russia.

As you can see from GFMS statement, they even included the word ‘Massive’ to describe the demand coming from India. I emailed Andrew Leyland, GFMS silver analyst and author of the report, to see if he could put some figures behind the declining U. K. silver inventories. He was nice enough to respond today by stating the following:

The LBMA itself doesn’t hold any silver stocks, but its member companies do. These stocks may be unallocated or allocated (often allocated to ETF holdings) and GFMS survey these stock levels once a year ahead of the silver survey in May.

What we’ve heard so far in 2014 has been anecdotal, that there have been large drawdowns in the UK of unallocated material. This has been backed up by trade data that has seen India increasingly buying from China and Russia while the UK (as the traditional lead supplier to India) has lost market share. While we can’t quantify the drawdown or stock level at this point we thought it worth mentioning the trend. In addition, for the silver survey, we’ll be trying to survey how much material from European bullion stocks is allocated. Silver ETFs holdings have been robust, in comparison to gold, and this could effectively limit available inventory to the silver market moving forward.

This post was published at SRSrocco Report on November 24, 2014.

US Stocks Surge To ‘Best’ Streak In 86 years

The last few weeks have been the strongest and most consistent rallies in US equity market history. US equity markets have traded above their 5-day moving average for 27 days – the longest such streak since March 1928 (h/t MKM’s John Krinsky) and all amid GDP downgrades, missed PMIs, and downward earnings outlook revisions. Given the holiday week, it is hardly surprising volume was weak today. Stocks were very mixed today with Russell 2000 and Nasdaq leading the way (along with Trannies) as Dow and S&P showed very small gains – to record highs though. Bonds were also bid with a strong 2Y auction extending the drops in yields (0-2bps) led by 7Y. The USDollar fell 0.4% – led by EUR strength – as JPY, CAD, and AUD all weakened. Despite USD weakness, oil (big drop intraday), copper, and gold also dropped on the day with silver ending 0.25%. VIX dropped to 12.66 – its lowest close in over 2 months.

The last few weeks have been the strongest and most consistent rallies in US equity market history. US equity markets have traded above their 5-day moving average for 27 days – the longest such streak since March 1928 (h/t MKM’s John Krinsky) and all amid GDP downgrades, missed PMIs, and downward earnings outlook revisions. Given the holiday week, it is hardly surprising volume was weak today. Stocks were very mixed today with Russell 2000 and Nasdaq leading the way (along with Trannies) as Dow and S&P showed very small gains – to record highs though. Bonds were also bid with a strong 2Y auction extending the drops in yields (0-2bps) led by 7Y. The USDollar fell 0.4% – led by EUR strength – as JPY, CAD, and AUD all weakened. Despite USD weakness, oil (big drop intraday), copper, and gold also dropped on the day with silver ending 0.25%. VIX dropped to 12.66 – its lowest close in over 2 months.

This post was published at Zero Hedge on 11/24/2014.

It’s Decision Time For Gold, Miners, And The Dollar

Last month we saw this chart–in which the swings in the GoldxUSDX index had formed a triangle going back over a year. At that time we were quite close to the apex.

Last month we saw this chart–in which the swings in the GoldxUSDX index had formed a triangle going back over a year. At that time we were quite close to the apex.

The last few weeks have been eventful. We saw a clear break below the lower trendline, followed by a bounce up above the upper trendline. It appears a decision has been made.

This post was published at Zero Hedge on 11/24/2014.

Smacking a skunk with a tennis racket

[Editor’s note: This essay was penned by Tim Price, a London-based wealth manager and editor of Price Value International.] On Monday 15th November 2010, an open letter to Ben Bernanke was published:

[Editor’s note: This essay was penned by Tim Price, a London-based wealth manager and editor of Price Value International.] On Monday 15th November 2010, an open letter to Ben Bernanke was published:

‘We believe the Federal Reserve’s large-scale asset purchase plan (so-called ‘quantitative easing’) should be reconsidered and discontinued. We do not believe such a plan is necessary or advisable under current circumstances. The planned asset purchases risk currency debasement and inflation, and we do not think they will achieve the Fed’s objective of promoting employment.’

Among the 23 signatories to the letter were Cliff Asness of AQR Capital, Jim Chanos of Kynikos Associates, Niall Ferguson of Harvard University, James Grant of Grant’s Interest Rate Observer, and Seth Klarman of Baupost Group.

Words matter. Their meanings matter. Since we have a high degree of respect for the so-called Austrian economic school, we will use Mises’ own definition of inflation:

‘..an increase in the quantity of money.. that is not offset by a corresponding increase in the need for money.’

In other words, inflation has already occurred, inasmuch as the Federal Reserve has increased the US monetary base from roughly $800 billion, pre-Lehman Crisis, to roughly $3.9 trillion today.

This post was published at Sovereign Man on November 24, 2014.

Swiss Gold Referendum: What It Really Means – Paul Craig Roberts

In a few days the Swiss people will go to the polls to decide whether the Swiss central bank is to be required to hold 20% of its reserves in the form of gold. Polls show that the gold requirement is favored by the less well off and opposed by wealthy Swiss invested in stocks. These poll results provide new insight into the real reason for Quantitative Easing by the Federal Reserve and European Central Bank.

In a few days the Swiss people will go to the polls to decide whether the Swiss central bank is to be required to hold 20% of its reserves in the form of gold. Polls show that the gold requirement is favored by the less well off and opposed by wealthy Swiss invested in stocks. These poll results provide new insight into the real reason for Quantitative Easing by the Federal Reserve and European Central Bank.

First, let’s examine the reasons for these class-based poll results. The view in Switzerland is that a gold backed Swiss franc would be more valuable, and a more valuable franc would increase the purchasing power of wage earners, thus reducing their living costs. For the wealthy stock owners, a stronger franc would reduce Swiss exports, and less exports would reduce stock prices and the wealth of the wealthy.

The vote is clearly a vote about income shares between the rich and the poor. The Swiss establishment opposes the gold-backed franc, as does Washington.

This post was published at Paul Craig Roberts on November 24, 2014.

Blistering Demand For 2 Year Paper Send Entire Curve Tighter

If the sellside community was expected to side with the Fed and sell Treasury paper, especially near maturities, then today’s 2 Year auction, which just priced at a hot 0.542%, or 1.1 bps through the 0.553% When Issued, indicating more than ample demand for Treasury paper. Further confirming the demand was the surging Bid to Cover, which at 3.714 was the highest of 2014, and the most since December’s 3.767. The internals too showed demand across all buyer classes, with Directs taking down 16.2%, Indirects getting 35.83% of the auction and Dealers left with 48%, or just a fraction below the 12 month average.

If the sellside community was expected to side with the Fed and sell Treasury paper, especially near maturities, then today’s 2 Year auction, which just priced at a hot 0.542%, or 1.1 bps through the 0.553% When Issued, indicating more than ample demand for Treasury paper. Further confirming the demand was the surging Bid to Cover, which at 3.714 was the highest of 2014, and the most since December’s 3.767. The internals too showed demand across all buyer classes, with Directs taking down 16.2%, Indirects getting 35.83% of the auction and Dealers left with 48%, or just a fraction below the 12 month average.

This post was published at Zero Hedge on 11/24/2014.

24/11/2014: External Debt Maturity Profile: Russia H1 2015-H1 2016

I covered recently Russian capital outflows data (see here:Now, lets take a look at the data for External Debt maturity profile for the economy. The reason for why this is of importance is that currently Russian enterprises and banks (even those not covered by the sanctions) have effectively no access to dollar and euro funding in international markets, making it virtually impossible for them to roll maturing debts. Chart below shows the quantum of debt maturing over the 18 months between January 2015 and through June 2016. The total amount of maturing external debt to be funded by Russian state, banks and enterprises is USD138.796 billion.

I covered recently Russian capital outflows data (see here:Now, lets take a look at the data for External Debt maturity profile for the economy. The reason for why this is of importance is that currently Russian enterprises and banks (even those not covered by the sanctions) have effectively no access to dollar and euro funding in international markets, making it virtually impossible for them to roll maturing debts. Chart below shows the quantum of debt maturing over the 18 months between January 2015 and through June 2016. The total amount of maturing external debt to be funded by Russian state, banks and enterprises is USD138.796 billion.

This post was published at True Economics on November 24, 2014.

Auto Loan Delinquencies Surge 18% Among Young Americans

Auto loan delinquency rates jumped nearly 13% in the last year, according to a new report by Transunion, with young (under-30) Americans seeing a 17.8% surge in 60 day delinquency rates, as auto loan debt rose for the 14th straight quarter to $17,352. While these are notable rises, the overall levels remain low for now, but subprime-loan-delinquencies rose notably to 5.31%. However, in a somewhat stunningly blinkered conclusion, Transunion’s Peter Terek notes “the uptick in delinquency reflects a healthy and thriving auto finance industry where credit is more broadly available to all consumers.”

Auto loan delinquency rates jumped nearly 13% in the last year, according to a new report by Transunion, with young (under-30) Americans seeing a 17.8% surge in 60 day delinquency rates, as auto loan debt rose for the 14th straight quarter to $17,352. While these are notable rises, the overall levels remain low for now, but subprime-loan-delinquencies rose notably to 5.31%. However, in a somewhat stunningly blinkered conclusion, Transunion’s Peter Terek notes “the uptick in delinquency reflects a healthy and thriving auto finance industry where credit is more broadly available to all consumers.”

This post was published at Zero Hedge on 11/24/2014.

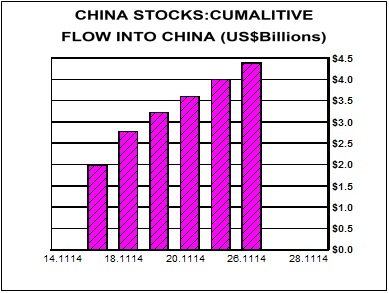

China…Follow The Money!

On morning of 17 November, while Western investors were sleeping, China opened the door to its investment world. On that day China began two way trading between the Shanghai and Hong Kong stock exchanges. This development essentially opened the Chinese stock market to investors around the world through Shanghai-Hong Kong Stock Connect. They said to investors around the world, ‘Welcome, just bring your money and come right in.’

On morning of 17 November, while Western investors were sleeping, China opened the door to its investment world. On that day China began two way trading between the Shanghai and Hong Kong stock exchanges. This development essentially opened the Chinese stock market to investors around the world through Shanghai-Hong Kong Stock Connect. They said to investors around the world, ‘Welcome, just bring your money and come right in.’

Investors would be well advised to be aware of the money flowing into the Chinese stock market, and possible ramifications of that money movement. Money is like water flowing across the earth, it fills in the low spot. To foreign investors, and in particular dollar-based institutional funds, the Chinese stock market is a ‘low spot’ to be filled in with money. Foreign investors will fill that ‘low spot’ with their money. Institutional money managers cannot ignore the most important economy in the world, and one destined to be the largest. As the chart at right portrays, the cumulative dollar flow into China’s stock market is off to a good start. At present the daily limitation on investment money inflow is 13 billion Yuan, or roughly $2.1 billion, per day. Actual money flows have been below that limit, but it is just the first week of the rest of time. Note especially that we only have a week of data, and the discussion that follows is about trends that will unfold over time.

This post was published at Gold-Eagle on November 24, 2014.

Here Are The Most Popular “Hedge Fund” Stocks in The Third Quarter

As observed last week, 2014 will be the sixth (and record) consecutive year in a row in which the hedge fund community will generate lower returns than the S&P. Worse, as of November 19, the average hedge fund was down year to date, which explains why as Reuters reported last week, there has been a deluge of redemption requests into the 2 and 20 space, assuring that this bonus season may be great for M&A bankers, but it certainly will be a disappointment to the lofty remuneration expectations of the vast bulk of hedge fund workers.

As observed last week, 2014 will be the sixth (and record) consecutive year in a row in which the hedge fund community will generate lower returns than the S&P. Worse, as of November 19, the average hedge fund was down year to date, which explains why as Reuters reported last week, there has been a deluge of redemption requests into the 2 and 20 space, assuring that this bonus season may be great for M&A bankers, but it certainly will be a disappointment to the lofty remuneration expectations of the vast bulk of hedge fund workers.

Furthermore, as we also showed, in the new normal, in which the market’s Chief Risk Officer(s) are all economist graduates of either Princeton or MIT, and congregate at the BIS HQ in Basel every few months to plot the future of the world’s centrally-planned economy, the best strategy has been to do the oppositeof what hedge funds have done: something we first observed over two years ago, as the most shorted companies have outperformed the vast majority if not all traditional strategies year after year.

And yet, just like the lunacy of believing that central banks are “fixing things”, when the current global economic situation is getting worse by the day precisely due to central bank policies, there are those pattern-chasing momos, who still find delight in copycatting whatever it is that the if not smartest, then best paid men, in the room do. For their benefit, here via Goldman, is the most recent, Q3, summary of the most popular stocks within the hedge fund community.

This post was published at Zero Hedge on 11/24/2014.

Follow on Twitter

Follow on Twitter

Recent Comments