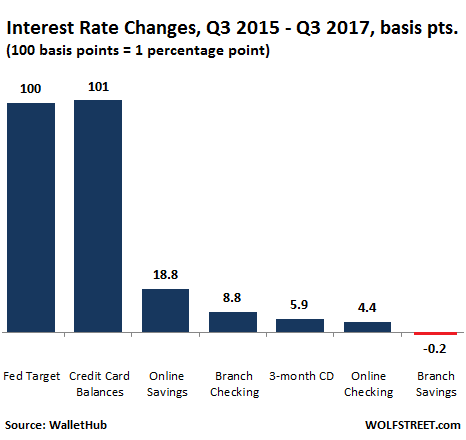

But savers are still getting shafted.

But savers are still getting shafted.

Outstanding ‘revolving credit’ owed by consumers – such as bank-issued and private-label credit cards – jumped 6.1% year-over-year to $977 billion in the third quarter, according to the Fed’s Board of Governors. When the holiday shopping season is over, it will exceed $1 trillion. At the same time, the Fed has set out to make this type of debt a lot more expensive.

The Fed’s four hikes of its target range for the federal funds rate in this cycle cost consumers with credit card balances an additional $6 billion in interest in 2017, according to WalletHub. The Fed’s widely expected quarter-percentage-point hike on December 13 will cost consumers with credit card balances an additional $1.5 billion in 2018. This would bring the incremental costs of five rates hikes so far to $7.5 billion next year.

Short-term yields have shot up since the rate-hike cycle started. For example, the three-month US Treasury yield rose from near 0% in October 2015 to 1.33% today. Credit card rates move with short-term rates.

Mortgage rates move in near-parallel with the 10-year Treasury yield, which, at 2.39%, has declined from about 2.6% a year ago. Hence, 30-year fixed-rate mortgages are still quoted with rates below 4%, and for now, homebuyers have been spared the impact of the rate hikes.

This post was published at Wolf Street on Dec 11, 2017.

Follow on Twitter

Follow on Twitter

Recent Comments