First of all, my brothers, I wanted to let you know that things will all soon be fixed in the contractual, derivative silver and gold markets! You heard me correctly, things will be made ‘right as rain’, and all those responsible for helping the fraud and rigging within these markets will be brought to justice! Wanna know why? Well, look no further than this latest announcement by the CFTC!

First of all, my brothers, I wanted to let you know that things will all soon be fixed in the contractual, derivative silver and gold markets! You heard me correctly, things will be made ‘right as rain’, and all those responsible for helping the fraud and rigging within these markets will be brought to justice! Wanna know why? Well, look no further than this latest announcement by the CFTC!

Washington, DC – The U. S. Commodity Futures Trading Commission (CFTC) today launched CFTC SmartCheck, a new national campaign to help investors identify and protect themselves against financial fraud. The comprehensive campaign includes a new website, a national advertising campaign and interactive videos that will help investors spot investment offers that are potentially fraudulent. The new website, SmartCheck. CFTC.gov, unveiled today, is an educational tool that helps investors conduct background checks of financial professionals.

Yes, the CFTC has redoubled their efforts to protect us all from financial fraud, God bless them! Why, they’ve even made a brand new website to help check the backgrounds of financial professionals! You see, this is crucial, because once the investing public uses this new ‘SmartCheck’ system on each member of the CFTC itself, they will discover that this organization has protected massive cons and market rigging in the commodity and precious metals spaces, by the largest investment and bullion banks on earth! Once citizens realize it, they will demand multiple arrests within the CFTC, and that law-makers shut down this shell organization for good!

Whew, and not a moment too soon, either! About time someone made this exceptionally helpful tool available to the investing public! Finally, justice for every regulator who has colluded with the banks, starting with the inventors of SmartCheck itself!

Onto the Matter at Hand

Ahh, ok, that’s enough Holiday humor! Ya know, sometimes ya gotta laugh to keep from weeping, as they say. In this case though, I suspect some of you may have laughed so hard that you did weep!

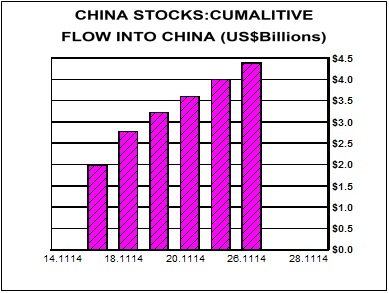

Recently, I took some time to highlight the silver investment demand numbers in India, because the figures we’re seeing there have staggering implications for every stacker. I’ve been watching India like a hawk because, believe it or not, their attitude toward silver is what largely holds the immediate present for precious metals in its hands.

This post was published at The Wealth Watchman on NOVEMBER 24, 2014.

Auto loan delinquency rates jumped nearly 13% in the last year, according to a new report by Transunion, with young (under-30) Americans seeing a 17.8% surge in 60 day delinquency rates, as auto loan debt rose for the 14th straight quarter to $17,352. While these are notable rises, the overall levels remain low for now, but subprime-loan-delinquencies rose notably to 5.31%. However, in a somewhat stunningly blinkered conclusion, Transunion’s Peter Terek notes “the uptick in delinquency reflects a healthy and thriving auto finance industry where credit is more broadly available to all consumers.”

Auto loan delinquency rates jumped nearly 13% in the last year, according to a new report by Transunion, with young (under-30) Americans seeing a 17.8% surge in 60 day delinquency rates, as auto loan debt rose for the 14th straight quarter to $17,352. While these are notable rises, the overall levels remain low for now, but subprime-loan-delinquencies rose notably to 5.31%. However, in a somewhat stunningly blinkered conclusion, Transunion’s Peter Terek notes “the uptick in delinquency reflects a healthy and thriving auto finance industry where credit is more broadly available to all consumers.”

Follow on Twitter

Follow on Twitter

Recent Comments