PE firms win again. Stiffed creditors not amused in bankruptcy court.

PE firms win again. Stiffed creditors not amused in bankruptcy court.

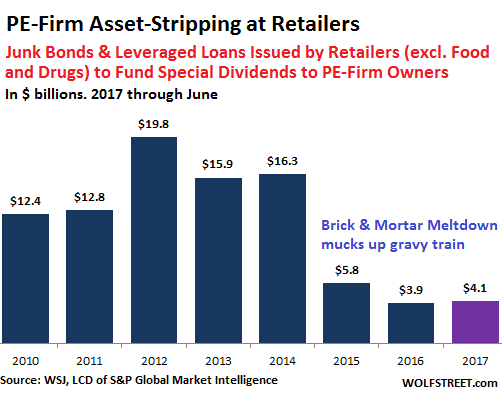

Nearly every retail chain caught up in the brick & mortar meltdown is an LBO queen – acquired in a leveraged buyout by a private equity firm either during the LBO boom before the Financial Crisis or in the years of ultra-cheap money following it. During a leveraged buyout, the PE firm uses little of its own capital. Much of the money needed to buy the retailer comes from debt the retailer itself has to issue to fund the buyout, which leaves the retailer highly leveraged.

The PE firm then makes the retailer issue even more junk bonds or leveraged loans to fund a special dividend back to the PE firm. Come hell or high water, the PE firm has extracted its money.

Then the PE firm charges the retailer hefty management fees on an ongoing basis.

This form of asset stripping removes cash from the retailer and leaves it struggling under a load of debt. It works wonderfully until it doesn’t – until booming online sales started eating their lunch, sending these overleveraged retailers, one after the other, into bankruptcy court, where creditors learn what it means to end up holding the bag. But they’re not amused, as we now see. But first the numbers…

This post was published at Wolf Street on Jul 31, 2017.

Follow on Twitter

Follow on Twitter

Recent Comments